Asia’s office market in 2026 is entering a significant transition as financial institutions increasingly follow talent rather than traditional financial-center dominance, according to a new report from commercial real estate services firm Colliers.

The study, which analyzed more than 200 financial-services markets worldwide, found that the region’s future office demand is increasingly being shaped by where banks, insurers, asset managers and fintech firms can access highly skilled workers in technology, artificial intelligence and data science rather than simply where capital markets have historically been concentrated.

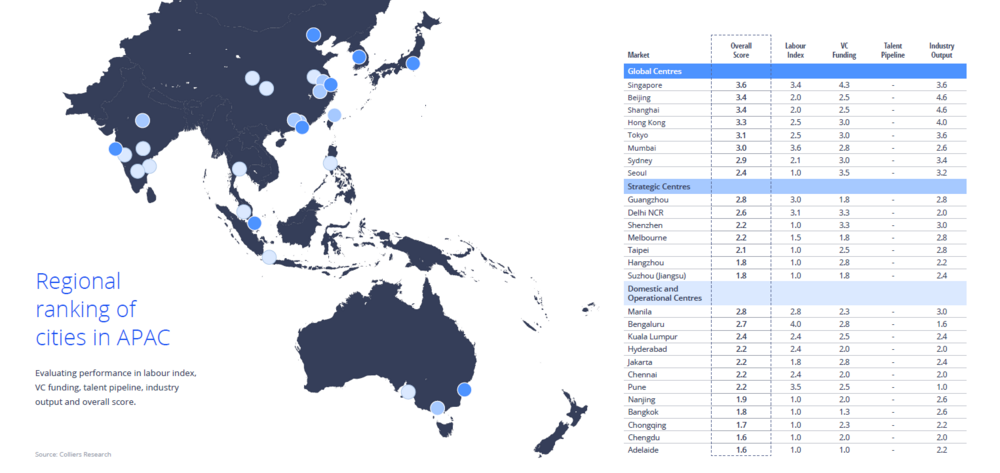

The findings point to a gradual reordering of Asia’s office landscape, with established financial hubs such as Singapore, Hong Kong, Tokyo, Beijing and Shanghai facing growing competition from emerging talent centers across India, Southeast Asia and Greater China.

Singapore remains Asia-Pacific’s leading financial-services market, while Beijing, Shanghai, Hong Kong and Tokyo continue to rank among the region’s most influential financial centers. These cities retain substantial advantages in capital formation, regulatory infrastructure, institutional investment and corporate headquarters activity.

Yet some of Asia’s fastest-growing financial-services labor pools are increasingly located outside the traditional gateway markets.

Indian cities including Delhi NCR, Mumbai, Bengaluru, Hyderabad and Pune have emerged as major financial employment centers, attracting investment from global banks and fintech firms seeking access to deep pools of software engineers, data scientists and AI specialists. Similar momentum is occurring in Shenzhen, Guangzhou and Manila, where expanding technology ecosystems are creating new opportunities for financial-sector growth.

Artificial intelligence is accelerating the shift.

As financial institutions automate functions ranging from compliance and customer service to risk management and payment processing, executives are reassessing where work is performed and what types of office environments are needed. Many tasks that once required expensive central business district locations can increasingly be performed from lower-cost markets, provided firms have access to highly qualified talent.

For office landlords and developers, the implications are significant.

Prime office districts in Singapore, Hong Kong and Tokyo are expected to remain critical command centers housing senior executives, institutional investors and major financial decision-makers. Demand for premium office assets in these locations is likely to remain resilient given their strategic importance to global capital flows.

However, some of the strongest future leasing growth may emerge in cities that historically played secondary roles in global finance.

Financial firms increasingly compete for AI engineers, cybersecurity experts, quantitative analysts and software developers. As companies expand in markets where those workers are concentrated, office demand is shifting toward modern, amenity-rich environments designed to support collaboration, innovation and talent recruitment rather than large-scale administrative operations.

Hybrid work is adding another layer of complexity to corporate real estate decisions. Many financial institutions are balancing return-to-office expectations with employee demands for flexibility, leading occupiers to reassess both the size and geographic distribution of their office footprints. In many cases, firms are consolidating headquarters space while simultaneously expanding operations in lower-cost growth markets.

Venture-capital investment trends reinforce the outlook. Singapore remains the region’s dominant fintech funding hub, while markets including Seoul, Shenzhen, Delhi NCR, Taipei and Manila continue attracting increasing levels of startup investment. Historically, rising venture funding has served as a leading indicator of future hiring growth and office absorption as emerging companies scale.

The result is a more distributed financial-services ecosystem across Asia. While landmark towers in Singapore’s Marina Bay, Hong Kong’s Central district and Tokyo’s Marunouchi will remain among the region’s most prestigious business addresses, much of the next decade’s office demand growth may come from emerging financial and technology corridors stretching across India, Southeast Asia and Greater China.

For investors, developers and landlords, the message is becoming increasingly clear: the future geography of office demand in Asia will be determined not only by where capital resides, but by where financial talent chooses to live and work. That shift, according to Colliers, is likely to become one of the defining forces shaping the region’s office markets over the coming decade.